Understanding Health Insurance Deductibles

Insurance

|

May 13, 2026

health insurance deductible, copay vs coinsurance, understanding health insurance

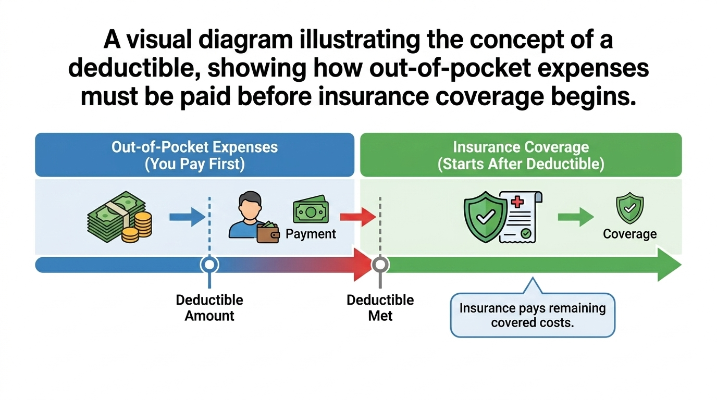

A deductible represents a critical aspect of health insurance, defined as the amount you are required to pay out-of-pocket for medical services before your insurance provider begins to cover any expenses. For instance, with a health insurance plan that carries a deductible of $1,000, you must pay this amount yourself before your insurance company steps in to share the costs of your medical care.

Recognizing the significance of deductibles is vital, as they directly influence your overall healthcare costs and decision-making processes. Many patients experience confusion surrounding deductibles, often mixing them up with copayments and coinsurance, which are common terminologies in insurance policies. This misunderstanding can lead to unexpected medical bills, underscoring the necessity of a clear grasp of how deductibles function in practical settings.

In this article, we will provide an in-depth exploration of deductibles, detailing their operations, different types, common misconceptions, and illustrating these concepts with real-life scenarios. Our goal is to equip you with the knowledge necessary to navigate your health insurance plan more effectively.

What Is a Deductible in Health Insurance?

A deductible in health insurance refers to a specified amount you must pay out-of-pocket for healthcare services before your insurance begins to contribute financially. For example, if your deductible is set at $1,000, you will need to be accountable for the initial $1,000 of your medical expenses. This includes payments for various healthcare services such as doctor appointments, laboratory tests, and hospital stays.

Most health insurance plans reset their deductibles on an annual basis. Once you have reached this threshold within the policy year, your insurance comes into play, starting to cover a portion of subsequent medical costs. For example, after meeting the deductible, you might only need to manage copayments (a fixed fee per service) or coinsurance (a percentage of total costs) for any additional medical treatment required.

For a clearer understanding, consider a scenario where you need treatment costing $2,500. You would first pay your deductible of $1,000, leaving a remainder of $1,500. If your policy includes a 20% coinsurance after the deductible, you would then cover 20% of that remaining balance—amounting to $300—while your insurance pays the remaining $1,200. Grasping the function of deductibles can significantly improve your budgeting for healthcare expenses and aid in selecting the optimal health plan for your lifestyle.

How Does a Health Insurance Deductible Work?

Understanding how a health insurance deductible works is essential for efficiently managing your healthcare expenditures. Here’s a step-by-step breakdown of the process:

Step-by-Step Breakdown:

- Initial Payment: Each year, you are assigned a specific deductible amount—say, $1,000. Until you reach this figure by spending on eligible medical services, you are responsible for paying the total out-of-pocket costs.

- Reaching the Deductible: If you conduct a visit to your physician costing $200, you bear the entire expense as it contributes toward your deductible. Next, should you undergo a lab test priced at $300, you will pay this as well, summing your total to $500 towards the $1,000 deductible.

- Insurance Benefits Kick In: After reaching the $1,000 limit for covered services—say, if a minor surgery costs $600—you will then begin to see your insurance cover a portion of future expenses.

- Cost-Sharing: Once the deductible has been met, a cost-sharing agreement often comes into play, referred to as coinsurance. For example, if your plan specifies a 20% coinsurance, you would take on 20% of any additional medical service charges, while your insurance manages the remaining 80%.

Real-Life Example:

To provide context, envision that throughout the year, you engaged in several medical events: a doctor check-up costing $200, a lab test costing $300, and a hospital bill for $600. The total of $1,100 surpasses your $1,000 deductible; hence, your insurance begins to take effect. For additional services, such as an outpatient procedure costing $800, you would be liable for 20% ($160), and your insurance would cover 80% ($640), fundamentally lowering your financial burden while ensuring you stay covered.

Types of Health Insurance Deductibles

Health insurance deductibles can take various forms, each significantly influencing the amount you pay out-of-pocket prior to insurance coverage commencing. Understanding these types can guide individuals in selecting the best plan for their specific needs.

Individual vs Family Deductibles

Individual deductibles apply to each person covered under a policy, meaning that once an individual meets their deductible, their insurance begins to cover their medical costs. Conversely, a family deductible amalgamates the total expenses each family member must incur before the plan provides coverage. Typically, meeting individual deductibles does not liberate other family members; they still have their respective deductibles unless a family deductible is in place.

Embedded vs Non-embedded Deductibles

Embedded deductibles allow for individual deductibles for each family member within a family plan. Once one individual reaches their deductible, their insurance coverage starts, even if the total family deductible has not yet been satisfied. On the other hand, non-embedded deductibles require the entire family to meet the collective family deductible before coverage is accessible for anyone. This crucial distinction can dramatically impact your out-of-pocket costs.

High Deductible Health Plans (HDHPs)

High Deductible Health Plans (HDHPs) are characterized by elevated annual deductibles and minimized premiums compared to traditional health plans. These plans empower consumers to have more control over their healthcare expenditures. Notable advantages of HDHPs include reduced monthly payments and eligibility to contribute to Health Savings Accounts (HSAs), allowing for tax benefits when saving for medical costs. Nonetheless, it is important to weigh whether you are prepared for potentially higher out-of-pocket costs should unexpected health issues arise.

Why Deductibles Matter When Choosing a Health Plan

Understanding deductibles is vital when selecting a health insurance plan. A deductible, as mentioned, is a critical financial metric. Its value plays a significant role in determining your overall healthcare costs. Generally, health plans with lower monthly premiums are coupled with higher deductibles, while those with higher premiums offer lower deductibles.

The trade-off between premiums and deductibles is significant for financial planning purposes. Consumers must assess their specific healthcare needs and anticipated expenses to determine how high a deductible they can manage comfortably. For example, if frequent medical attention is expected, opting for a lower deductible with a potentially higher premium may be beneficial to minimize out-of-pocket costs during times of need. Conversely, individuals in good health may prefer a plan with a higher deductible and lower premium to save money long-term.

Ultimately, it’s essential to strike a balance between risk and cost. Analyzing both your expected healthcare usage and financial landscape is crucial in selecting the right health plan, ensuring that you remain prepared for any unexpected medical expenses.

Common Misunderstandings About Deductibles

Misconceptions surrounding deductibles frequently lead to confusion among consumers. A prevalent misunderstanding is equating a deductible with the monthly premium of a plan. It’s essential to clarify that these terms denote different concepts: while a deductible reflects the amount paid out-of-pocket before insurance contributions begin, a premium is the ongoing payment required to maintain coverage.

Another common myth is that having a deductible implies you won’t receive coverage until it’s met. In reality, many health insurance plans provide coverage for specific medical services even when a deductible is unmet; preventive care services, for example—such as vaccinations and annual check-ups—may not require the deductible to be paid first, ensuring you access vital health services without immediate costs.

Recognizing these misconceptions empowers consumers in navigating health insurance policies with confidence, leading to a clearer understanding of their costs and responsibilities.

Real-Life Example Scenario

When assessing different health insurance plans, analyzing the financial ramifications of a low deductible versus a high deductible can significantly inform your decisions. Let’s examine two fictional individuals:

- Person A has a plan with a low deductible set at $500 but faces a higher premium of $400 monthly, accumulating an annual cost of $4,800. Should Person A engage in medical services totaling $2,000 in a year, their total expenses would equal $4,800 (premium) + $500 (deductible) = $5,300.

- Person B opts for a high-deductible plan with a $3,000 deductible but benefits from a lower premium of $250 monthly, leading to an annual cost of $3,000. If Person B incurs $2,000 in medical services, they would be responsible for the complete $2,000 due to the heightened deductible. Coupling this with their premium results in an annual expenditure of $3,000 + $2,000 = $5,000.

This comparison highlights the financial trade-offs involved: while Person A pays more in premiums, they mitigate their out-of-pocket expenses more significantly during medical needs. Conversely, Person B enjoys lower monthly costs, but must brace for higher significant expenses before insurance benefits commence. Grasping these dynamics empowers consumers to choose health insurance options that align with their financial positions.

Final Reflection on Deductibles

In summary, understanding deductibles is vital in the realm of health insurance. They shape how individuals access healthcare and influence overall medical expenses. A deductible is the initial out-of-pocket payment made before insurance coverage activates, significantly impacting financial responsibilities for healthcare services. By offering insights into the various types of deductibles and their roles in health insurance, individuals are better prepared to make informed choices. High deductibles may yield lower monthly premiums but could also trigger substantial out-of-pocket expenses when serious medical needs arise. Thoroughly reviewing and comprehending one’s insurance policy and deductible structures is essential for planning healthcare expenses strategically. Equipped with this information, readers can navigate their health coverage more effectively, ensuring alignment between their medical needs and financial situations.

Was this helpful? Share your thoughts